Housing in the US has gotten to where it is due to horrible laws effectively allowing total tax avoidance for landlords.

Take some investment property. You buy it at some basis price, let's say 500k. You rent it out for 15k a year. Each year you can offset your rental income against deprecation of the property and property taxes - meaning, you pay no income tax on your rental income.

~30 years later, you've deprecated it down to an effective value of $0, so you hypothetically would have to start paying taxes on your rental income(of course, you can still deduct property taxes against that). What do you do? Well, there's something called a 1031 exchange - this lets you sell an investment property, and as long as the funds go directly into another investment property, you pay no capital gains taxes. So guess what? You can buy a brand new investment property with a new(albeit adjusted) cost basis, and you can start the entire cycle of depreciation and deduction all over again on your new, more expensive, property.

So, you've now held this property your entire life, and you die and pass it to your kids - well, great news, unless your estate is over 12 million dollars(and double that for a married couple), you pay no estate taxes. And even more fun - when you inherit property, the cost basis is "reset" to the present day value of the property at time of inheritance - So your children can now rent the property out, deprecate it, and pay no income tax on the rental income either, and continue the cycle.

The net result is that rental properties generate a ton of income for the owners, who pay almost nothing in taxes. Even if they do pay property tax, property tax rates are generally much lower than income tax rates.

You don't write off your rental income. You depreciate the rental property over 27½ years and write that off against your rental income. Few rental properties will have under a 3.7% ROI where depreciation would cover all the income. At best you might be paying half tax. In your example, you'd pay no tax, but you'd lose out on the potential income you could have had with better investments (and lose about 6 years' worth of depreciation by the depreciation then being too fast).

And flipping to more and more expensive properties through 1031s requires more and more capital and only makes it cover less taxes. There's no tax benefits versus just keeping the first property and paying all the taxes and buying a separate property to depreciate.

If you sell a $500k property earning $40k/year where the depreciation covered 45% of your income, and you buy a $1 million property earning $80k/year, you get a new $500k to depreciate $18k/year. Then the depreciation only covers 22% of your income.

Depreciation is very fundamental to business tax law. I'm not sure how you'd "fix" that without penalizing non-rental companies for expanding.

You're skipping over the (extremely important) part where you take out a mortgage on property.

So you buy the $500k property with $125k in cash and a $375k mortgage (25-30% down is typical for investment mortgages). Depreciation *plus mortgage interest expense* leads you to (for tax purposes) more or less break even on this investment after 10 years and so you pay no tax.

After those 10 years are up, you've now paid off around $68k of the principal, plus the asset has gained $250k in value. So from your initial $125k of capital invested, you now have ~$400k in capital that you can leverage into a $1.6M property in a 1031 exchange. That bigger loan comes with a much larger mortgage interest expense, so you continue to earn no taxable income while growing a larger and larger asset and taking a (relatively modest) cash-on-cash return.

This is very common. We have it in Norway too. It started in 1882. At that time, it was mainly farmers who had mortgages, so the idea was to encourage productivity, making it less costly for them to buy new land for cultivation (You might wonder, wouldn't this just drive up land prices? I wonder, too.)

But once you have them, they're hard to get rid of. When they were in charge for 40+ years, Labour defended them because they wanted to push for homeownership so working people didn't have to live at the mercy of landlords. In the 80s I believe they considered changing it, but then the Conservatives (who of course benefit disproportionately from the deduction) were in a position to block it. These days there is an interest deduction on ALL loans, not just mortgages. Why and how that happened I have no idea.

The deduction of business mortgage interest payments is still always less than the money you lose by having to pay interest. Paying cash will always make you more money than a mortgage unless you have something else to do with the cash.

That doesn't change my point that the only way you can pay no tax is to have less than a 3.7% ROI before mortgage principal payments.

Again, that's a bad investment. If they put the money in the stock market or a better real estate market and got a 7% return, that would be 60% higher, even after taxes.

Sure, you build equity in the properties, but you'll have to pay all those taxes you've been putting off if you ever try to use that equity. I guess the kids could sell it before they depreciate it, but I can't imagine who would intentionally waste the potential of their money so they don't have to pay the (low) capital gains tax. Again, you'd make more money paying taxes on any almost investment making over 4.3%.

This is certainly not my area so I could be missing something basic. But after you sell a property, why shouldn't that force a reevaluation on past depreciation writeoffs? In idkyall's post, they mention the scenario of depreciating your property down to an effective value of $0 and then selling to buy another property to start again. You've argued that this only covers a fraction of your income. But at a basic level, if you get enough from the sale to buy a new property, then the old one must have been worth much more than $0 so one was wrong for decades about claimed depreciation ... right? In which case, it seems like it should be natural and fair to have to pay up on taxes from those previous years.

If I can invest in real estate, rent it out for decades, and then sell it at a significant profit (which seems to be the case in many in-demand cities), then why should _any_ amount of that rental income get a to be balanced against imaginary depreciation?

What you describe does happen, unless they use that transfer process described, but by doing so they reduce the effective cost basis of the new property by the difference between the cost basis of the old one and the sale price.

Yeah, I guess the unintended? consequence here is that the lack of a time window allows indefinitely propagating it, maybe the exchange should come with a time window phase out.

We need a third party to validate both of your claims, because I don't know where to start to understand who is right. This is an example of someone (me) who wants to understand the issue, but would need to google for days to understand both arguments.

The rebuttal by mminer237 is much closer to right [0].

Also it isn't even as good as mminer237 mentions, as many states also have a much lower exemption, and there is work in congress to get rid of the step-up in basis (a bad thing, imo) and to reduce the $12MM lifetime gift & estate exemption (a very good thing).

So yes, there are some advantages, but OP is vastly exaggerating as if it is some freebie to landlords when it is not. There were some freebies introduced in the bills in the Trump term for the type of LLCs that Trump runs, but IDK if they were fixed in legislation in this term.

If you want a general complaint, perhaps the angle is that capital is taxed much less than labor, under some notion that lower taxation is necessary to get people with capitol to actually deploy it in investments. I think that is provably false, and certainly does not require the level of tax code favoritism it currently enjoys.

[0] source: tax & estate attny at biglaw firm in the household, although this is just from info absorbed by osmosis over years and is NOT a detailed legal analysis.

It may not be a freebie for landlords, but it is much more "cost neutral" or "tax neutral" to own an investment property than to own a primary residence. Consider:

Investment property:

* Deduct maintenance costs

* Deduct insurance costs

* Deduct property taxes

* Deduct mortgage closing costs

* Deduct mortgage interest

* Deduct HOA dues

* Deduct property management fees

* Take advantage of depreciation deductions

* Avoid paying cap gains taxes on sale using 1031 exchanges

Primary residence:

* Deduct property taxes (only on federal taxes, and only up to $10k, assuming you don't have other SALT to deduct)

* Deduct mortgage interest (only up to a loan value of $750k)

* Avoid paying up to $250k in cap gains taxes on sale

Doesn't that seem incredibly lopsided to you? The current tax regime makes it very attractive to own an investment property, but a basic need -- housing! -- doesn't give you much in the way of tax breaks. And the breaks that are there, are capped.

Of course there are more deductions when an object is a BUSINESS instead of a piece of PERSONAL PROPERTY.

No, it does not seem the slightest bit lopsided.

There is zero difference between the deductability of expenses you mentioned and expenses for any other business.

Businesses are generally taxed on their PROFITS, which are [INCOME] MINUS [COSTS].

The regular homeowner is not running a business.

The same thing is true of a truck or racecar. If you own it as personal property, you don't get to deduct much of anything. If you own it and run it as a business, you can deduct your expenses before counting profits and paying taxes.

The same object can be either a personal property or a business, and it is the ACTIVITY that matters, not the object.

Your argument is either attitude & ignorance gone wild, or demagoguery attempting to confuse the issue with sleight of hand.

If you think that home ownership should be more subsidized than just the mortgage interest deduction, just say so and advocate for those subsidies. It'd be much more cogent, but you evidently don't want that discussion, or expect it to be a loser, which it likely is.

> Businesses are generally taxed on their PROFITS, which are [INCOME] MINUS [COSTS].

Sure. But why does it get such a sweet deal?

It's because we want to encourage business, since businesses produce things of value.

But how much does a landlord actually produce things of value, and how much is he just extracting value others are producing (a.k.a "rent")? That's an important thing to consider when we look at having this tax/tax break or not.

The distinction between extractive vs value-creating profits is very important.

That said, it's not automatically a "sweet deal", and identifying that difference is nontrivial. The same activity could be one or the other, depending on how it is done. Your example with a landlord is particularly thorny:

>>But how much does a landlord actually produce things of value, ...?

A good landlord creates a building from nothing, and maintains it in good condition for his/her tenants. What was an undeveloped parcel of land is now homes for all the families who live there. Considering all of the people yelling about lack of housing, that is something of real value. Even maintaining a building in good condition is a very expensive activity, and if the maintenance is not done, the homes will certainly revert to rubble.

So that good landlord is absolutely creating, for both his renters and society at large, serious value.

OTOH, a bad landlord doing superficially the exact same activity can be completely extractive - merely collecting rents and failing to maintain the building(s) in any way beyond what will keep them out of immediate trouble. The bad landlord extracts everything they can for current cashflow and allows the building(s) to degrade towards rubble, an anti-creative activity.

One is definitely creating value that is highly needed in our society, and the other is destroying and extracting it, yet both have the same business type, both have the same income and cost structure, etc..

Even more difficult, the same landlord can look like one or the other in different times - in high-demand times and/or markets, they can charge premium rents and profit while still doing lots of maintenance & upgrades, but in a down market, they may have high vacancy, and still lose money while doing the absolute minimum.

So, how do we tell the difference and tax them differently?

That's a serious question, and one which, if we can find an answer will really help the society improve.

Rent extraction from the underpriveleged for basic needs in a deliberately skewed market is hardly "business", it's raw exploitation at the systemic and the social level. Justify your habit of cannibalism however you may.

If I buy a widget for $100,000 and sell it of for $105,000 do you expect me to pay income taxes on the $105k or on just my $5k profit?

The former would be absurd and in most cases would make it impossible to be in business-- you'd take a net loss on every transaction unless your markup was greater than your tax rate. Good that went through fewer hands would be astronomically less expensive.

So why do you think that it's weird that a landlord doesn't pay taxes on the portion of his income that goes to the costs of operating the business?

> If you want a general complaint, perhaps the angle is that capital is taxed much less than labor, under some notion that lower taxation is necessary to get people with capitol to actually deploy it in investments.

Yes, I recall when cap gains taxes dropped significantly during GWB and was, sadly, happy. Of course, I was just a dumb 20-something and didn't realize how much of boon to the wealthy it was.

Please point to the "boon". If you mean people got to keep their jobs = boon, then I guess you are right. The problem is, wealth was transferred upstream, en masse, and not taxed anywhere near labor.

Here is some data that solidly debunks your disguised claim of "trickle down":

> It's a boon to anyone whose job was created by it as well

You then say:

> If you mean people got to keep their jobs = boon

No, I said the job in the first place is funded by investment. I couldn't have made it clearer.

If investors don't invest in your startup/scaleup then there is no job in the first place. Nothing about being grateful for keeping your job.

> The problem is, wealth was transferred upstream, en masse, and not taxed anywhere near labor.

You're thinking in terms of groups instead of individuals, and that the groups are static. You shouldn't (as it will lead to so many broken ways of thinking) and they aren't.

> Here is some data that solidly debunks your disguised claim of "trickle down"

It's not trickle down - I only go for nonpolitical theories, and the US left wing's labels to oversimplify and demonise some fairly standard economics doesn't hold up by that measure.

I'd rather you replied to what I said than straw man it. You will mislead casual readers by doing so.

It contains the ASSUMPTION that the favorable capital tax rate (vs labor tax rate) is NECESSARY for the investment to happen.

This is obviously not the case. People with capital will want to deploy it so that it grows, as long as the tax rate on the profits is <100%.

What we do not have is the curve - how high can the tax rate be set relative to the tax on labor income before investment is ACTUALLY discouraged?

Only an assumption, based on the obviously self-serving assertions of people who own capital, that higher tax rates will make them just sit on their money and not deploy it profitably.

As you can see above, I'm happy to debunk oversimplification & demonization from the LW or RW, but "trickly down" is pretty much what the RW called it when it was flogged as a concept in the '80s, that "freeing up capital" for the rich would trickle down to everyone in the economy. The ACTUAL result was the opposite. Ratios of executive vs worker pay only increased from ~70x to over 300x, and the share of the total GDP going to labor declined to the lowest point ever.

The actual fact of the matter is that with lowering tax rates on capital, the "boon" you speak of is actually available to fewer people than ever.

> The ACTUAL result was the opposite. Ratios of executive vs worker pay only increased from ~70x to over 300x, and the share of the total GDP going to labor declined to the lowest point ever.

You're assuming a cause effect relationship. The far more likely causes of this are automation (allowing more work done by machines than people) and globalisation (allowing reach of larger markets).

That's the mechanisms. As for the philosophy: I don't buy the idea that a CEO getting richer hurts me. What's important is that my standard of living is better than my parents', and my children's will be better still. If someone wants to risk it all for a big win then good for them. They will probably fail, and lose years off their life, but occasionally they will succeed. Only pointing at the people whose risk-taking paid off and saying "See!" is not a good way to understand (or communicate) the full picture of what's going on when people invest or run their own company.

Do we actually have strong evidence that these sorts of tax breaks actually stimulate this kind of economic activity to the degree where it's actually worth it?

It... doesn't seem like we do? I mean, it's not like pre-1990 we had skyrocketing unemployment and underinvestment in business, and lowering capital gains taxes fixed it.

Yes, the question is how much of a boon it needs to be.

The fact of the matter is that people with capital want to invest and grow that capital. It is absolutely false that if that activity is taxed, it will disappear. Just as obviously, if all capital gains are taxed at 100%, it will disappear. The question is the balance - how much to tax it so that the wealthy don't merely get wealthier at everyone elses' expense.

It may also be a good idea to tax underutilized capital, as land is taxed.

If you get all of that just right you may even extract enough money to pay for all the many governmental systems required to administrate it. Sadly none of that will have done anything as useful as an investment in a company that makes people's lives cheaper or better.

ummm, the mortgage interest deduction does NOT apply to rental properties, only your primary residence or a 2nd home that you spend at least 14 days or >10% of the time you rent it out. So, if you are talking about a fully rental property, it is incorrect.

I'm not saying that there are no advantages or deductions, only that this character is trying to portray it as the govt basically giving landlords all the funding to become landlords. If that were the case, he should simply do it — there's plenty of no/low money down ways to get into it —, but I notice that he is not doing it. It just smacks of a lot more attitude than fact.

This is already the case. You can only depreciate the building value not the land portion. So single family homes have much lower depreciation since most of the value is typically in the land vs an apartment which is the opposite.

> Since for most properties the majority of the value is in the land itself

I'm not sure that's the case for the majority of the country. At-least it's not here in my greater metro area (suburbs or rural... yuppie downtown areas... perhaps, but again, downtown is not majority for most places)

It may be not true right now amid difficulty in finding labour and materials. Much like cars, the value of a used home is proportional to the cost of building a new home. When new homes are difficult to acquire, cost of used homes go up. Used cars have also increased in value lately for the same reason. This is not typical, however. These are normally depreciating assets.

Under usual market conditions, houses are headed to being on the older side and reaching the end of their effective lifetime, leaving little value left in the structure. You can renovate a home to bring it back to new-like condition, which restores value to the structure, but that cost must be maintained in the equation.

I'd think anywhere where apartments are viable to build it would be true, and of course large rural properties. Whether they make up "most properties" I'm not sure - it would surprise me if much less than half of properties in Australia were sitting on land worth more than the house itself (despite the enormous amount of undeveloped/low-value land we have!).

When you are the owner/user and not the landlord you should be paying the taxes because most of the taxes are for use in the local community and most of that is schooling. The landlord gets no benefit from the majority of that stuff. The tenant does.

How does he benefit from the rental property? He doesn't live there an use the services. If he lives somewhere else in the town he pays taxes based on that. He charges rent for the other location to cover the taxes because he doesn't benefit from those taxes. The renter does.

But he passes the cost of those taxes on to the renter because the renter is the one benefiting from the schools/roads/police/fire/etc that the taxes fund.

That is often true. A vacant rental still owes the taxes though. I can only say my time as a landlord I have not always covered those costs with rental income. Sometimes the property is empty or doesn't command enough income to cover all your costs.

I actually don't understand why the laws are written that way, apart from the political goal of causing W2 workers ("suckers") to bear a disproportionate tax burden. A W2 worker incurs expenses that are necessary to earn their income, including food, transportation, clothing, and healthcare. If they were able to account for these necessary expenses as a business does, the expenses would be directly deducted from income.

And that's not even getting into the S-corp self-employment-tax dodge.

For one, no, those expenses aren't deductible even if you do itemize. They're considered "personal expenses" even though they were necessary to earn that W-2 income. If you buy a car and use it at least 50% to get to 1099 client(s) you can deduct that portion of it (including accelerated depreciation). But if your income is coming from W-2 job(s), you simply cannot.

For two, the standard deduction is better seen as a personal exemption (which it subsumed), giving everyone a level of income that they don't have to pay tax on. Especially given that business expenses generally flow through as direct subtractions regardless of the standard deduction.

There is definitely tension between allowing deductions to account for actual income fairly, and the resulting (de facto) requirement that everyone do minutiae accounting for their personal finances.

Unless your property taxes are over $20K per year, you can? It's just most people don't because their standard deduction is greater than what they have records for itemizing. https://www.thebalance.com/property-tax-deduction-3192847

The link you provide points out the SALT deduction cap of $10k. With the standard deduction up to $12k+ now, if your only itemized deduction is your property and state income taxes, itemizing isn't going to be worth it.

We were so close to losing the cap on SALT deductions with the Inflation Reduction Act; I'm super bummed it didn't make it into the final bill.

I think the only long term solution is a federal land and building tax. This is too important to leave to states (and definitely local) governments. A high tax with no credits, deductions, exemptions.

Then, from this tax, we can pay "forward" every adult tax payer (not children, only adults) a fixed amount that pays the cost of an imaginary nationwide median cost of a two bedroom unit. Only adults, all adults, regardless of whether you have no child or eight children. Must file a federal income tax return to qualify. Median nationwide cost somehow calculated and weighted by population, hopefully updated more than once a decade.

Everybody from Amazon.com to Walmart pays this land + building tax regardless of whether they are in Manhattan, New York or Deport, Texas. No exceptions.

Well yes but that's also the case with property taxes. A reasonable figure based on current market values seems simpler to calculate for unimproved land than it does for property tax, which includes the value of the unimproved land as well as everything else built or changed. And because it's the value of the _unimproved_ land it's based on, the value would be relatively stable over time as well as not varying much between one area and similar areas nearby, whereas property taxes are based on values that can change dramatically over time from one place to the next, which can lead to mis-valuations and general stress from constant changes.

Aside from a 1031 you can do what I do and take loans against the property to buy the next property. Keeps your tax basis lower. At least in LA county the appreciation is limited to 2% a year while the increase in property value has been 20%+ the last few years.

You can do this indefinitely with commercial real estate including multi-family dwellings. Lenders are comfortable with 50% loan-to-value. You do need to have some cash flow from the properties to service the debt. It does require the properties to either appreciate over time or for you to build up more equity in them by paying down your loan.

You can do this indefinitely with commercial real estate including multi-family dwellings. Lenders are comfortable with 50% loan-to-value. You do need to have some cash flow from the properties to service the debt. It does require the properties to either appreciate over time or for you to build up more equity in them by paying down your loan.

> Depreciation is very fundamental to business tax law. I'm not sure how you'd "fix" that without penalizing non-rental companies for expanding.

You can fix it by only deprecating the original cost. A person who buys a 50 year old house shouldn't be able to depreciate a second time, (then next owner again)

"Few rental properties will have under a 3.7% ROI"

This is a leveraged investment (meaning you have a mortage). What that means is for your 20% down payment (the actual money you invest), that 3.7% writeoff on income can be an 18.5% cash on cash yield (ROI) in which you pay no taxes, ever. Few properties on the market can get you a better yield than that. If your ultimate yield is less than that you can roll those losses over year over year, so that then later if/when you get more yield you still* don't have to pay any taxes. It's a really big tax loophole and is the reason Donald Trump pays almost nothing in taxes (and he admitted as much in the presidential debate).

*I own 3 properties in buffalo, one of the best rent to value markets in the US, and it's hard to find better yield than that even in that market. https://simplepassivecashflow.com/rv/

Really the only problem here is the step-up cost-basis at death that you mention. This is indeed a big problem, and the fix is simple: Your heirs inherit your cost-basis as well (likely $0), so that when/if they sell it they have to pay taxes on the whole capital gain. We could also force the payments over some years, by increasing the cost basis and taxing on that amount. e.g. I inherit a property worth $1M and zero cost basis. After one year, I have to pay capital gains taxes on $100k, but my cost basis also goes up by $100k. Repeat each year up to $1M.

The other stuff (depreciation, 1031 exchange) are very sensible accounting. Depreciation applies only to the improvements (buildings) on the land, not the value of the land itself. This reflects genuine loss of value over time (buildings wear out). And in the event that you sell the property at a profit down the road, you have to pay back all that tax savings at higher regular income rates (not lower capital gains rates). This is called "depreciation recapture." So depreciation can defer taxes, but not eliminate them.

Likewise, when you do a 1031 exchange, your new property ends up with a lower cost basis based on the previous property, so that when you later sell it you still have to pay all that capital gains tax and depreciation recapture. It defers but does not reduce or eliminate taxes.

Of course - if you die while holding these properties, then your heirs get the cost basis reset ("stepped up"), which does indeed eliminate all these taxes. This is what we need to fix.

It provides a large artificial financial incentive to hold onto a property that you otherwise would sell.

I also think it's not right to create this kind of arbitrary, large tax break that only applies in specific circumstances. I think if we're going to have a capital-gains tax (and maybe we shouldn't), then we should keep it simple and not have carve-outs.

If I sell my house while I'm on my death bed, I pay all the taxes. If I wait a week to die first, and then my heirs sell, no tax. This is wrong and unnecessary.

I don’t know, I think there are a lot of people that might not want to be owners anymore, but they just can’t bring GM themselves to sell and pay the taxes. Especially if they are, say, 60 and in dubious health anyway. So they hold, and hold, and hold some more for decades. I could see my own parents on this situation possibly.

Or I have a neighbor house that’s a rental, but it’s still owned by the same (now) 90+ year old woman who used to live there, but who moved out 20 years ago. Her 70+ year old son is managing it now… Does she really still want to own this house, or is inertia and fear of taxes holding her back from selling? I don’t know.

When purchasing real-estate in a hot area, the real money comes from increasing prices. Some cities have had something like 10% - 15% annual growth, for 10 years straight.

Banks are also much more forgiving when it comes to down-payment, when they know it's going to be a rental, and you already have other rentals as collateral.

In essence, purchasing a rental unit with only 1%-5% down payment up-front, is kind of like purchasing stocks with 20x - 100x leverage. As long as you meet your mortgage payments, get steady rent, and don't get any crazy expenses - you're sitting on a goldmine.

Some of the guys I went to school with did just that. Bought a rental unit, while working. All their salary went toward down-payment of the next unit, and the banks were very forgiving when it came to new loans. After 10 years they had a nice portfolio of rentals, which they then sold to typical real-estate investment funds.

> Banks are also much more forgiving when it comes to down-payment, when they know it's going to be a rental, and you already have other rentals as collateral.

I don't think that's true. The interest rate on your loan will be more expensive if it's an investment property and the LTV requirements are more strict.

If the bank knows it's a rental, it's considered a commercial mortgage with a minimum of 25% down.

And if you're lying to the bank by saying it's a residence when it's meant for rental -- you've just committed fraud (it's one of the clauses in your mortgage).

As a former landlord for nine years, this is pretty correct. I did the tax deferred exchange thing once.

Then I sold for cash (a pretty big no-no in terms of real estate investing) because I didn't enjoy such a concentrated risk.

When I sold, there's something called depreciation recapture. If the 27.5 year depreciation thing was used to offset your income taxes, part of your gains gets taxed as ordinary income. The cost basis of property is also lowered so that the capital gains is higher.

There's also tax trick called cost segregation that lets you depreciate certain parts of your property at an accelerated rate.

Basically, as the OP says, keep doing the 1031 exchange until you're dead and your heirs don't have to worry about depreciation recapture.

And are losing value on the property, which is the point of depreciation.

>~30 years later, you've deprecated it down to an effective value of $0

An no one will now rent, since your building has an effective value of $0 since it has become crap.

All throughout your list you ignore all the costs involved in being a landlord. Have any friends that have tried it? (I do). Did they become silly rich? Or did they quit because it is a major problem to actually make it very profitable versus other uses of capital and time? I'm a decently saavy investor (in many things), and have watched multiple friends start up rental properties, only to stop once it became clear that tenants destroy things, costs to maintain properties are volatile and astronomical, the work required is significant, and so on.

I have done the math on real estate investing many times, and each time have decided the returns are not worth it.

>The net result is that rental properties generate a ton of income for the owners

If it were so profitable, then tons of capital currently being spent on other uses (tech, medical, finance) would instead go into buying up more housing. But the fact is that being a landlord is not very profitable, so capital doesn't flood into that market - it is still mostly elsewhere.

Historically, housing has performed quite similar to the stock market for returns - as it should be. If housing were a better investment, money would flow in until they balanced. If housing is too poor an investment by screwing with taxes, then money will flow out into other more productive places. And if money flows out, people wanting housing will then have to pay even higher prices for less stock.

>"Did they become silly rich? Or did they quit because it is a major problem to actually make it very profitable versus other uses of capital and time? I'm a decently saavy investor (in many things), and have watched multiple friends start up rental properties, only to stop once it became clear that tenants destroy things, costs to maintain properties are volatile and astronomical, the work required is significant, and so on."

I'm sorry but this flies in the face of my experience. Most landlords I have met buy properties and then outsource their administration to property management companies. I have never seen or spoken to my last three landlords, none of whom lived anywhere near the same city as the property.

Landlordism is parasitic in the literal sense of the word. Landlords get rent and capital appreciation for doing nothing but possessing an ownership title. The propertyless pay the propertied a premium to live.

In light of both those observations, I would say any enrichment in this case is "silly", and that landlords don't tend to do much - or any - work.

>"If it were so profitable, then tons of capital currently being spent on other uses (tech, medical, finance) would instead go into buying up more housing."

This is a non sequitur. If X is profitable and the market knows X is profitable then it should, in theory, be attracting exactly the amount of capital it merits already.

In the UK, where I live, the rental sector has exploded, jumping from 2.8 million households in 2007 to 4.5 million in 2017. [1]

>>Most landlords I have met buy properties and then outsource their administration to property management companies.

And the cost of buying a property and outsourcing its maintenance is 0 right?

The landlord magically pulls a home out of thin air and some group of people maintain for them for free?

>>Landlordism is parasitic in the literal sense of the word. Landlords get rent and capital appreciation for doing nothing but possessing an ownership title. The propertyless pay the propertied a premium to live.

This applies to any investment, including things like 401K, pensions, getting an education, or even taking care of one's health.

Why should anybody in an economy be better off than the other part of the population by being disciplined, making routine and early investments?

Good news is you can plan and start working to go over to the winning side by taking action on it today. Or you can call others 'parasites' for making smart decisions you don't make. Calling others names might mask your own failure, and downplay their achievements, but is unlikely to change anything for your or for them.

> The landlord magically pulls a home out of thin air and some group of people maintain for them for free?

The building-lord should receive some return for their investment, as they have created value and added to it through maintenance.

The land-lord receives return for doing no work, no addition of value, and only through extracting the excess economic rent from their tenants.

Unfortunately, conversations around property investment and land taxes and so on tend to derail because the land-lord and building-lord are often the same person. The response to "the landlord is a leech on society" is "no, he built a house and maintains it!", but in reality it is "the land-lord is a leech on society, the building-lord is a contributor to society".

Yeah, land, like college seats, and gym memberships come in limited quantities. There is no infinite supply of land, college seats, or gym memberships. So whoever acquires a hold on a resource of this nature stands to benefit a better return on investment. Also note the limited nature of time in these things, you are basically in a race condition.

Note these extend to things like 401k, or a retirement savings scheme in the same way.

You feel like you are salty that you couldn't get a hold on such a resource in time.

The difference between land (and natural resources) and gym memberships, 401ks etc. is that you can make more gyms and companies and investment fhnds, but the supply of locations and natural resources is limited. This means that land functions as a monopoly (hence the board game!) whereas 401ks and gyms are non-monopolistic.

Owners of monopolies stand to benefit from not just a reasonable return on investment, but an excessive return on investment proportion to their contribution to society.

Many countries and societies have handled this in different ways, such as the idea of the commons, or Norway's taxation of oil extraction, or land value taxes and land leases.

> You feel like you are salty that you couldn't get a hold on such a resource in time.

I am a software developer, and as such am able to comfortably acquire land in a good location and provide for my family. However, many of my generation are unable to, unlike previous generations, because the good locations have all been taken by the previous generations. This is why we see enormous poverty next to enormous progress, because late comers to the party are so far behind as to be basically unable to "get on the ladder". The ladder is being pulled up before their eyes.

A great solution to this is to tax the excess economic rents that monopolies create, rather than taxing labour and capital. Henry George is the most famous proponent of such a system, and you can find out more here: https://www.gameofrent.com/ or at astralcodexten's book review of Progress and Poverty.

This means that those who contribute to society through labour and capital are not discouraged from doing so, but those who leech off others through monopoly rent extraction return that rent to the society that created it in the first place. This is a far more just and equitable solution.

Of course, many existing monopoly owners (e.g. landowners, and particularly property investors) hate the idea, because people tend to act in their own self-interest to the disadvantage of others.

> any enrichment in this case is "silly", and that landlords don't tend to do much - or any - work

Hm - the same could be said about your 401(k), but you probably expect to live off of it at some point in your life, right? At worst, buying and renting properties is a (risky) investment.

And there was a housing crash in there and decent growth in population over that time.

Next, instead of picking a window wrapping the biggest housing bust in a century, pick various decades and see how normal volatility behaves - and you might find this variability not uncommon.

In fact, from your own source, Figure 1 - the percent of rented properties is, well, nearly constant over the entire window (31% rented in 2007, 37% rented in 2017). And somewhere in there mortgage laws got significantly tighter - no need for pesky investors to be the cause of less mortgages.

So go figure, right? Lots of reasons and complexity in there.

>"And there was a housing crash in there and decent growth in population over that time."

There was a slight slump in rentals after the financial crisis, not before. So if anything it would depress the subsequent growth. In England the population grew over that period from about 51 million to 55 million. That's a 7% increase. Privately rented households, as per the link I posted above, rose by 63%. Hardly compelling.

>"In fact, from your own source, Figure 1 - the percent of rented properties is, well, nearly constant over the entire window (31% rented in 2007, 37% rented in 2017). And somewhere in there mortgage laws got significantly tighter - no need for pesky investors to be the cause of less mortgages."

Figure 1 shows private rentals increase from 13% in 2007 to 20% in 2017. Social rentals, which you are bizarrely conflating with private rentals, refers to social housing, and is exactly what I think should take the place of landlords. So its decline reinforces my point.

>There was a slight slump in rentals after the financial crisis, not before

And a significant decline in mortgages over that time, likely due to mortgage law changes as a result of the crash. Making it slightly harder to get a mortgage would, over time, move people from mortgages to rentals, which is exactly what the data shows, right?

UK added Basel capital rules, the affordability test, and changed capital ceilings in banks, among other changes. Academic papers list these as being major drives in declines in UK mortgage rates. Those people rent instead.

All with no need for speculators to drive the market up - the laws changed.

>Social rentals, which you are bizarrely conflating with private rentals

Ah, so now we're only taking a subset of renters. Good idea.

> Most landlords I have met buy properties and then outsource their administration to property management companies.

Who do not actually pay for any repairs or upgrades to the property (that is the landlord's responsibility, and who in addition take an extra 5-20% of the rental upfront. Yes, it "outsources" actually dealing with the rental property and renters, but has no impact on the costs other than making them higher.

I know we like to give the benefit of doubt here on HN, but that crosses a line. Landlords are known to perhaps not take the best care of their property, but in general, even if a tenant totally trashes the place it isn't too hard to strip down whatever got abused and rebuild it. Same thing happened to us when we rented a property. Tenant did as much damage as you can imagine with pets and abuse short of ripping wires and pipes out of the walls. It was really annoying to fix, but not hard. In the [late] 2020 real estate market it was easy to sell it and the house appreciated like 30-40K since we sold it easily.

To claim that you need to spend money equal to the tax-assessed value of the building over the course of 30 years to maintain equal value is slightly less ridiculous, but still not exactly reasonable. The (conservative) rule of thumb is 1% of the property value per year in repairs, which would be 30% of the property value over 30 years. And even then, it seems there's no shortage of fairly decrepit buildings that have no problem finding tenants.

Here is a starter list of things a house will need over the course of 30 years.

- a new roof (maybe two if they are 15 year rooves)

-new siding (unless fiber cement siding was installed originally)

-new exterior paint

-new windows

-major repairs to the driveway

-2 new furnaces

-2 to 3 new water heaters

-2 to 3 full new sets of appliances

-1 cosmetic kitchen remodel

-1 cosmetic remodel of each bathroom

-1 to 2 cosmetic relandscapings

-1 to 2 new floors (depending on the flooring material chosen)

-new exterior doors

-new garage doors and openers

None of this includes any repairs the home may have needed at the time of purchase. Nor does it include any upgrades. Nor does it include any unexpected repairs that may not be covered by insurance (there are many). Nor does it include any of the dozen or so minor repairs you either have to do yourself or get a handy man for.

I'm not going to symp for the landlords but maintaining property is brutally expensive. I know because I bought a 40 year old house. Since I bought a home I've become very convinced that there are a ton of landlords losing their ass out there. Some have been saved by the ridiculous property valuations we've seen lately. But that is not the norm. Houses typically increase in value at a pace with inflation.

Personally, I would only ever rent housing I had specced myself because the design choices and material choices have a huge impact on the cost of maintenance.

Factors also depend on the age of the house and your location - harsher climates are much worse on various house factors.

A new house will have much less costs to maintain over 25 years than a 50 years old house.

Having owned a few houses (both relatively new), and having gfs with houses and seeing the stuff they've done, and with helping my mom and sister with their house decisions and fixing, the list above is not far off.

State Farm says to budget 1-4% of the value of a house for annual upkeep costs. You're significantly below that it sounds.

> State Farm says to budget 1-4% of the value of a house for annual upkeep costs. You're significantly below that it sounds.

Certainly far below, maybe like 0.1%

Although basing it on the market value doesn't make much sense since housing prices cycle wildly up and down, whereas maintenance just increases with inflation.

>To claim that you need to spend money equal to the tax-assessed value of the building over the course of 30 years to maintain equal value is slightly less ridiculous, but still not exactly reasonable.

No one wrote that either. You're reading what you want to argue into what is written yet again.

> which would be 30% of the property value over 30 years

Ignoring increasing property value, compound interest, opportunity cost, that plenty of places put this between 1 and 4%, and that pretty much all places indicate the rate increases as the property ages, and that this rate is for owners whereas tenants are statistically worse on property, then sure.

For example, State Farm [1] recommends between 1% and 4%, which would vastly increase your estimate. And tenants are statistically worse on property than owners

In reality it's a far larger cost over 30 years than 30% of the original price.

Why would it not be rentable? That’s an assumption that doesn’t stand on its face when you look at the unmaintained crackhouses landlords will rent easily because demand is so high for housing.

Does >0 money spent equal 100% deprecation over 30 years?

If the landlord spends a single penny in paint does that make up for getting an asset that’s considered zero value but still gets to be sold for hundreds of thousands?

Are you aware of the concept of risk? The amortization schedules are what they are for a reason, even if not all houses only last 30 years, the average is what matters here.

Any number of things can result in houses being destroyed and become worthless prior to that time, including damage from earthquakes, fires. Additionally poor initial building standards, or changing building standards, or new regulatory barriers can make certain properties become not just worthless, but have an active cost to their owners and therefore have negative value.

I'd say the truth is somewhere in between. It is really, really not that great unless you have some superbly well located shiny great apartment in Manhattan or some other center center which gets 100% short term rental ie airbnb. But then this is multi-million $$ property.

Long term rentals - the gains are minimal given how much capital is completely locked in that property and not doing anything else. If you are lucky, you have long term nice tenants and stuff generally doesn't break (ie heating/wash machine bursting and flooding everything, including 5 apartments below). If unlucky, 1 bad accident that needs to be fixed asap will wipe out any income you have for given month, if not more.

Utterly random example - I got locked out (if thats the proper term) last sunday evening, went for a walk and big weird key wasn't turning in our old very massive (15cm thick & heavy) doors that look like they could handle a nuclear blast. Called some emergency services for this and they opened it, but showed me the lock basically disintegrated and I was lucky they didn't have to drill huge hole in those doors to get in and pay tripple the cost. The cost for new lock in those doors with all work? 2400 Swiss francs (cca 2500$), and that was work week rate of one of the cheaper agencies doing this, albeit in Geneva, one of the most expensive places to live. For a freaking lock that is just old design, fitting some 50 years old doors. Guess who pays that? Well me but I will get 100% reimbursement from agency who will get it from owner.

Properties are great if you inherit them and suddenly have a nice passive income (and management worries). Or if you are lucky with timing and in 10 years they jump 3x with value. Thats over now. I wouldn't invest in properties now unless its for primary residence and then a lot of emotions and other concerns come into equation, but financially its not great.

$2500 isn't that far off of the monthly rent for a single apartment in a lot of American cities. Sure, your old door might need a new lock after 30+ years (although given it was 15cm thick I'll bet it was much older than that).

> And are losing value on the property, which is the point of depreciation.

The house depreciates while the land appreciates. In the US for the last 50 years has been net appreciation for most homes.

> If it were so profitable, then tons of capital currently being spent on other uses (tech, medical, finance) would instead go into buying up more housing.

Hedge funds have been buying houses at scale since the great recession.

> Historically, housing has performed quite similar to the stock market for returns

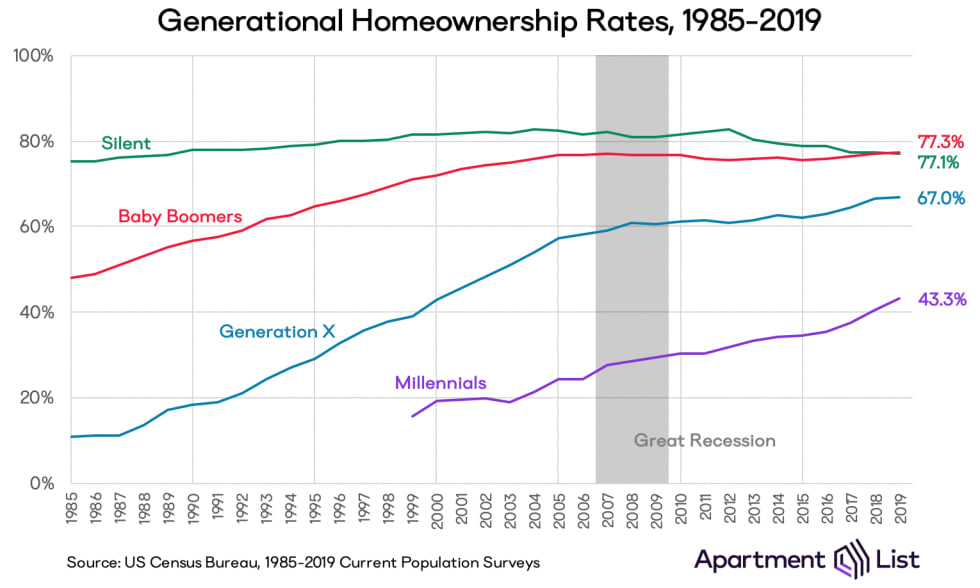

Which increases faster than incomes. Hence the way each generation has a declining rate of home ownership.

>Hedge funds have been buying houses at scale since the great recession.

Zillow tried that and lost over a billion dollars - I'd expect lots of those purchases are not the money makers you think they are.

>Which increases faster than incomes.

Not for the same size houses - the median house now is many times the size of a median house from 1950, and a few times the size of a median house from 1970. If you buy the same house previous generations bought, you'd find prices relatively the same.

>Hence the way each generation has a declining rate of home ownership.

That's not what historical data shows [1,2], going all the way back to 1900. Each generation has had higher ownership rates at equal points in life than each previous one, except perhaps a recent one due to the 2008 crash, but they're catching back up again.

Certainly there is no way you can claim each generation declines and see the same data FRED and Census post.

For example, FRED shows that Q2, 2022, at 65.8% is higher than all of history except the decade before the crash, and it is trending up again.

Anecdotally, the price per square foot has also gone up in the places with the most jobs. To be clear, the whole context of the article is that we're talking about the (sub)urban areas that have seen substantial job growth. If zoning prevents large houses from being split then you're describing an increase in mansions while others can't afford a home.

Despite younger people moving to less prosperous regions where they can afford a home, yes, home ownership rates for younger generations have declined. Specifically, in the family and peak earning years from 30 to 50.

https://ipropertymanagement.com/research/homeownership-rate-...

"An no one will now rent, since your building has an effective value of $0 since it has become crap."

This isn't true. You will have put money into the property to keep its value up, also writing off all of those expenses, so that you can still rent it out.

>You will have put money into the property to keep its value up

You're ignoring what was written: if the building has value 0, then it is not maintained to keep the value up. Of you kept the value up, then it would not have an effective price of 0.

Of course most people put money into properties exactly to keep value up.

>also writing off all of those expenses

Writing off expenses does not make them free - you are still paying for them - out of otherwise profit. It just means you get taxed on net profit instead of taxed on property gross income. But you are still losing money.

Writing off expenses is not some free money giveaway.

The point was to illustrate that OP ignored costs involved for landlords in the thought experiment.

oh it's certainly not free money (queue the seinfeld episode of kramer telling jerry to "write it off") but the discussion is about taxes or lacktherof. In no other investment that I know of are you allowed this double write-off: you can write off both the investment as it depreciates and the costs to make sure it doesn't depreciate.

That's a list of how long until the landlord can file an eviction, not how long an eviction takes.

"Thus, the eviction process can take from five weeks to three months, assuming there are no delays. If there are delays, the process can take as much as a year."

It is easy to pick an example like this to show the “bad” sides. But what is the alternative? If people had to pay inheritance tax on their family home, how many could not afford such a tax bill and would have to get rid of their family home to please the tax man.

Regarding the cost basis rest that is so people can upgrade their house without having to pay a tax bill. This is just deferring the tax not avoiding it. Without this it would be much harder to get a bigger house once you have kids. Most people would have a harder time moving and removing this would lower our quality of life.

> If people had to pay inheritance tax on their family home, how many could not afford such a tax bill and would have to get rid of their family home to please the tax man.

so if they can't afford to pay tax on the windfall, they'd have to sell the house and buy a smaller one. is that the end of the world?

> Regarding the cost basis rest that is so people can upgrade their house without having to pay a tax bill

what they have in many european countries is that you can do this only on your primary residence. so you let people upgrade their homes, but not their rental properties

If you had to pay the tax you could probably just finance it anyway instead of paying it all at once so it would be just like having a new (small) mortgage.

Now the US is way ahead of the game here compared to Europe. There are no property taxes in most of Europe and families hang on to their homes for generations.

I know for a fact (through living here) that Denmark and probably the rest of Scandinavia has property tax and inheritance tax -- holding on to family property is almost as expensive as buying new property.

Which part of Europe are you referring to? I once had Greek colleague who complained about having to maintain three generations worth of houses, so that might be one place where things are as you describe?

Right, Europe is bound to be diverse on this point. I have exposure to Balkan countries and the UK (which, while they do have non-zero rates, still have them far lower what I'm used to in New England).

I think you can argue migration (forced) through history is tied to this. The US was a recent star in growth due to free land. But there is no more free land. And Mars does not fill that role. We need to disempower rentiers.

Wouldn't this just reduce land entitlement for those who aren't wealthy enough to afford the new taxes? I think something like taxes that apply for people who own more than 1 property would be better.

I mean, we can solve that problem by a 100% inheritance tax so they don't leave an obligation. No? Then maybe let's skip arguing in sound bites.

Personally, I think the answer here is a continued and ongoing land tax. Occupying land should come with an expectation you contribute to the common good, because you don't "own" land. It's a shared good, just like air and water, and you should pay for use.

Primary residences should indeed not be subject to an inheritance tax - if they are continued to be used as a primary residence. Providing an ongoing home for a family unit[1] is a societal good, we shouldn't punish it.

[1] Definition of family is a hairy problem for another, longer post.

I know reasoning skills are hard, but here, let me help you: OP posted a snarky comment. I proposed a policy. Feel free to bring arguments debating the policy.

So a family on hard times should be forced to leave their grandmothers home when she dies and hope they can find a new one? Gentrification can easily push a property in the place they've lived their whole lives out of their price range. And the family home might not have been super well kept up so the "windfall" isn't as big as the property values in the area may reflect. This happens now with gentrification in big cities, it would get worse with what you are saying.

Being able to leave something to your descendants is a critical part of society. If people know they cant leave anything behind they start acting differently (and not in a good way). I understand a key part of communism is you and your family own nothing, but trust me you don't want people to have a use it or lose it attitude towards everything.

Yes, if you can't afford your house you need to find a new one. The family will come out well ahead here because the tax would only be on a percentage of the houses value, they can use the proceeds to buy a new, cheaper house. No one has the right to live anywhere just because their grandma did.

>Private property, to a communist, is not your shoes or toothbrush, or even your house.

>Those things are called personal property and under socialism and under communism they continue to belong to workers in much the same manner as they do now.

Criticize people for what they actually believe, not what you imagine they believe.

I can't defend any particular policy of any particular place. I don't think I would call myself a communist, either. But restricting land ownership is a common feature of technocracy in dense urban environments. I seem to recall that the UK does something similar. Even in the US, when you "own" a condo, you are subject to various liens and easements, and can under certain circumstances be forced to sell. China, being rather crowded, likely has created policies to manage land availability.

Communism is, primarily and essentially, about the end of money. Other features of socialist countries are largely the result of how some theorists planned to achieve communism, although they invariably fail. (Some people insist on adding "so far".) Some communists on Quora directly addressed the question of homeownership here:

Somehow, all kinds of unrelated policies get called "communism" or "Marxism", even when they directly contradict what Marx said (e.g. restrictions on gun ownership). I don't think it's helpful to policy debates to have this syncretistic demon hanging around appropriating the bad name of communism.

Assuming that's true (I have no knowledge of how Chinese real estate works), then that's because China is an authoritarian country that has decided it wants to control every aspect of citizens' lives. That can be a feature of any economic system, if the government is powerful enough, and has nothing to do with communism.

> I understand a key part of communism is you and your family own nothing

As I understand, a key part is coming to the realization you and your family have already been robbed (or evicted to go back to your example), and then to ask what's next? At least as I understand Marx, particularly in Capital v. III, the point is to construct a world in which poor & working class regain collective control of resources like food, shelter, health that sustain life. The abolition of transfer of private property is intended to end the cycle of extracted (stolen) life-sustaining resources ending up in the hands of the same family (or dominant group).

As a case in point, the theft of Black farm land has been well documented https://www.reuters.com/world/us/us-black-farmers-lost-326-b.... The point of communist organizing in Alabama during the 1930's -- detailed in Robin DG Kelley's "Hammer and Hoe" -- was to protect Black small farm owners from theft of their meager lands, and to take actions so that sharecroppers (tenant farm workers) could collectively control enough land to sustain themselves.

No. The estate tax doesn't start until the inheritance is over $12 million.

So they have to inherit a $12m estate before they're taxed, if it's less, no estate tax.

And they don't pay taxes on that $12m if they're over the $12m, only the amount that it's over that $12m. If it's worth $12,000,001, they pay taxes on only $1.

When you effectively take someone's home for government benefit. People think that when they buy property they own it. You're model is more the China version. You don't own property, you only lease it from the government. Hence, your model looks more like the communist model than the traditional Western one.

It's basically the American model - if somebody isn't improving their land, you take it from them by force and sell it at cheap prices to people who will.

That's why it's a bunch of white people with title now, rather than all being native americans

> It is easy to pick an example like this to show the “bad” sides.

You're saying this as if the example is a cherrypicked outlier rather than ubiquitous.

> If people had to pay inheritance tax on their family home, how many could not afford such a tax bill and would have to get rid of their family home to please the tax man.

At some point in the value of a home, we're not really worried about that. We do not sympathize when someone can't keep their parent's $50 million dollar home tax-free. We've set that cap at around $12 million. It's a very high cap.

edit: we're happy to grab the estates of working people who end their lives in intensive care, nursing homes and hospices, before the Medicare kicks in.

I think inheriting property should absolutely force children out of their home unless they plan to actually live in it as their primary home immediately, and even if they do, they should be paying the same taxes as the rest of the neighborhood.

> Regarding the cost basis rest that is so people can upgrade their house without having to pay a tax bill. This is just deferring the tax not avoiding it.

I think it's fine to allow this treatment for a home used as a primary residence for the exact reasons you mention, but I don't understand the logic of allowing it for an investment property

> Without this it would be much harder to get a bigger house once you have kids. Most people would have a harder time moving and removing this would lower our quality of life.

If the goal is to help people consume more of <x>, then give them cash.

Giving assistance via tax rules is a way to discriminate who gets to benefit from government subsidized while maintaining plausible deniability. It also helps obfuscate the costs.

>If people had to pay inheritance tax on their family home, how many could not afford such a tax bill and would have to get rid of their family home to please the tax man

If your family is leaving you a house worth more than $12 million, you can afford to pay the tax man.

> But what is the alternative? If people had to pay inheritance tax on their family home, how many could not afford such a tax bill and would have to get rid of their family home to please the tax man.

This is absolutely normal in the rest of the world, and there's nothing wrong with it. People don't go bankrupt over inherited property. The tax-free inheritance part is also ridiculous, in my humble opinion inheritance should be fully taxed.

a tax per square feet on residential properties where the owner doesn't live in for more than half a year, irregardless of wheter it's rented out or not, and independent from the tax from rent income. since "promoting good behaviour" trough taxation didn't work the last idk 50 years, it's time to be back to "punish bad behaviour"

How high would that tax bill be? 50-60%? Still would be lot under fair value of property and thus should be able to get loan against that tax amount. So I really see no reason not to have it taxed.

There's an argument that for inherited property, the cost basis should be zero since you didn't pay anything for it; you got it for free.

Although, that's effectively a tax on inheritance that's due at sale, which would probably be a fairly big incentive against ever selling, and instead structuring it as a long-term lease.

I'm speaking as someone who put all his retirement savings into index funds year after year, but then married someone whose job is related to real estate. Real estate feels more concrete and understandable to her than finance, so that's where our money goes now.

It's not easy free money, and I don't know why you would think that any high-profile, low-barrier-to-entry investment would be easy free money. Half of my friends have either bought property or are constantly talking about it. My friends are part of a horde of first-timers who believe, like you, that it's easy free money, and their belief inflates prices.

And that's not just my amateur opinion: my wife and I sit in on a developer happy hour where experienced developers constantly bemoan that they haven't been able to work with certain types of property in years, because they get outbid by naive first-time buyers who don't have a plan for making money other than betting on the market going endlessly up. People who are looking for income rather than appreciation are not seeing opportunities at the current prices.

Thanks to my wife managing our properties herself and having a lot of applicable skills from her profession, we manage to make some money, but every hour she spends managing property is an hour less (or two, really) that she can bill her clients. I doubt that if we adjusted for that it would work out to be a wise use of time. It's work she enjoys and finds satisfying, so we don't look that closely at whether her time (or our money) would be more profitably invested elsewhere, but I'm certainly not quitting my software development job to double our commitment to real estate.

I'm in Austin, one of the hottest markets in the country, so in the end, it's possible that everyone regardless of how naive they are will be rewarded by continued appreciation. Income from real estate hasn't been a game-changing multiplier for us, but appreciation might be. Or not. That aspect of it is just a gamble.

It sounds like you're landlords, but you didn't explicitly state it. But isn't your tenant basically paying off each property, over the next 30 years. So right now your debt load may be high, but you're not experiencing that. You're just paying off the loans from rental income and handling the overage (prop tax and fixes) with the dev job. So in 30 years the two of you will have like 40M dollars paid over the backs of renters by selling all those properties..

I mean that's fine, it's legal. But if that's the goal of real-estate, then of course it will never be affordable to the next generations. Everyone wants to do what you are doing.

Yes, we're landlords. We own two small properties that were originally built as residences but now have commercial tenants because the zoning permits it and therefore the tax valuations assume we'll use it that way.

> Everyone wants to do what you are doing.

As with any other asset that makes money, there are reasons why property prices are what they are, and if it's a magic ticket to free wealth, you have to ask yourself why professionals with deep pockets aren't grabbing every property and driving prices up even further. In the case of properties that are within the reach of upper-middle-class earners, professionals are not willing to pay the prices that overexcited individual amateurs are.

> isn't your tenant basically paying off each property

...and it's special logic like this that convinces people that there's free wealth to be had. But there's no magic. There is a price. There is income. There are costs. There are assets that depreciate. The land is an asset that appreciates. That all adds up to a return on the investment. Professionals calculate the return and compare that to other things they could do with their money.

Amateurs (like us) just buy and hope and feel good because we're doing something that feels like rich person stuff. We're doing fine with our properties, but we'd be doing fine putting our money into index funds, too. In case it's not clear, I don't think our properties will turn out to be great investments for us unless the speculative aspect pays off big. But my wife actually enjoys the work of finding tenants, handling building maintenance, designing and overseeing improvements, etc., so we implicitly price her time at zero.

Let me repeat that to let it sink it: I think we'd be just as well off putting our money in the stock market. The main reason we've put a significant amount of our money in real estate because my wife enjoys it and doesn't mind putting a lot of personal work into our properties for free.

> you have to ask yourself why professionals with deep pockets aren't grabbing every property and driving prices up even further.

But... they are.

My Experience

Ever heard of Grant Cardone? He and his ilk are filling my youtube algorithm with seminars on how to do this. I meet strangers on planes telling me about gathering together in clusters of partners and buying up real estate. Ads on the radio hawk house-flipping courses. Robert Kioysaki sells book teaching how to do this. With just a little bit of inherited wealth - and American wealth is 60% inherited - people are building multi-generational legacies.

Research

In Massachusetts:

> In 2021, business entities purchased nearly 6,600 single-family homes across the state, more than 9 percent of all single-family homes sold. That’s nearly double the rate of such purchases a decade ago, according to a GBH News analysis of data provided by the Warren Group, a real estate data analysis firm. [0]

In 2021:

>corporate investors snapped up 15 percent of U.S. homes for sale in the first quarter of this year [1]

In 2020:

> a company called Treehouse Group was folded into Blackstone, then renamed in 2012, Invitation Homes was on a $10 billion spree, purchasing $150 million worth of houses per week.

In 2022:

> About 2.5 million households shopping for a first home will be shut out of the market this year, estimates Nadia Evangelou, senior economist with the National Association of Realtors. That amounts to 15 percent of all first-time home buyers. In an already daunting market, investor purchasing is adding to the obstacles. [3]

> “The more that investors buy up entire communities and turn them into rental communities — people don’t have a choice anymore,”

Yeah but part of what throwaway908724 says is absolutely true:

There are a lot of naive newbies _and_ investors buying up property right now without a viable plan to ever make money on that property. This in turn drives up prices for both potential owners and "reasonable" landlords, then by extension for renters both because potential owners continue renting reducing supply and landlords need higher rent to break even let alone profit.

The worst is when investors stop maintenance on the property, it begins to deteriorate, then they write it off and bail. That turns what could have been a rehabilitation by a competent investor into a tear-down. More than a few apartment buildings are being ruined by this sort of thing, evicting all the tenants in the process.

> Ever heard of Grant Cardone? He and his ilk are filling my youtube algorithm with seminars on how to do this. I meet strangers on planes telling me about gathering together in clusters of partners and buying up real estate. Ads on the radio hawk house-flipping courses. Robert Kioysaki sells book teaching how to do this.

In those cases the professionals are making money using people's dreams of becoming wealthy to sell books and seminars. Learn the One Simple Trick to turn your high salary into lasting wealth that Wall Street doesn't want you to know.

In the cases you cited where corporations are buying homes, yeah, there are firms that do a lot of quantitative research and forecasting and identify homes that they think are underpriced according to their rental value, ignoring the vast majority of properties on the market. If you're in a community they've identified as being underpriced, I guess it can look like they're buying up the whole world, but it's a selective strategy, completely different from the blanket assumption that property is an easy doorway to wealth and riches. As one of those articles notes, they don't compete against "wealthy boomers and the nation’s finance and tech bros," because we're willing to pay silly prices for property. They buy in neighborhoods where people like us aren't looking.

Those professionals may be making money on the books and seminars, but those books and seminars have been sold to people that are snapping up homes for investment, don't play dumb about that.

I know 6 people who all got into real estate including myself. Almost all of us exited because it's way too much work for very little gains. I just invest in an index fund, much closer to free money, and no calls at 2 am in the morning about a busted pipe.

"It's not free money because it's more time consuming than the stock market!"

It's free money in the sense that you are getting paid for having had the money to buy the property. Your wife might be putting in the time, but she is not more expert than 90% of people who could live there and maintain the property just as well (assuming they didn't have to pay you rent and the police didn't come to enforce your "property rights").

And yes, that means the stock market is also free money.

Are you spending an unreasonable amount of time managing property vs the rent you take in?

I spend a max of an hour a month on average on property management. Find good tenants (reduce the rent if you have to). On average my tenants have had 3+ year leases with minimal management.

We've done significant remodeling between each tenant just to stay competitive with other properties coming on the market. Plus each tenant requests specific improvements for their business, so those need to be negotiated. Then you need to keep a close eye on construction, like every day on site, because it often happens that if the tenant is on-site with the contractors they'll try to get them to do things that you said no to.

Finding tenants has taken a significant amount of work as well. There are commercial brokers that act as matchmakers, but you still have to meet with the tenants, walk them through the space, talk about what kinds of modifications they want, figure out if the timelines are compatible, and do a little bit of due diligence. She does quite a few of these where the details don't quite work out because the tenant is looking for a different style of building, easier in-out for the parking, improvements we'd never agree to, etc.

The process of transitioning the properties to commercial was also time-consuming. Commercial has entirely different requirements, and upgrading the parking, accessibility, etc. took a lot of time, money, and back-and-forth with the city.

> unless your estate is over 12 million dollars(and double that for a married couple), you pay no estate taxes.

Why aren't estates just taxed as income to the entity who it goes to? If my father croaks and leaves me $1m it should count as an additional $1m of income to me that year.

"If my father croaks and leaves me $1m it should count as an additional $1m of income to me that year. "

If it is $1m in property value, do you count that as still $1m of income? If so unless the child is in great financial situation with a lot of already liquid cash, they would be forced to sell part/all of the property to pay the taxes.

If a parent croaks and has a small business, mom and pop style. How would that be handled? If they had a small corner store making 100k/profit but has no assets vs a shop that sells very expensive equipment making 100k/yr in profit. But has hundreds of thousand in assets that would pass down.

Fine, as long as you tax based on what was paid for the property. The father is giving his invested money, no one chose to 'realize' at the current valuation, it is happening because of a traumatic family event.