The timing of ATM chip deployment is determined by the region's rate of card fraud, not technological sophistication. There were significant transaction costs for the transition, and it made economic sense to roll them out sooner in places with higher rates for fraud, so, Europe before US. Not sure about how the rollout happened in Japan, but it makes sense that they haven't completed a transition given their very low crime rate.

This is factually incorrect on two grounds: First, the adoption of Chip & Pin in Europe predates the European Union. Second, credit card fraud in Europe, France in particular, was out of control before its adoption. I believe it was either a French or Swiss researcher that developed the technology in response.

My understanding is that French (and presumably other European) banks assigned the liability for fraud to the account holder, whereas in the US, liability for fraudulent credit card charges falls to the banks and the credit card processing networks.

This meant that individual account holders were much more tolerant of chip-and-pin technology, and demanded additional security features like portable card readers, which mean that the credit card never leaves the account holder's possession.

Do you have a source for this? Lite googling suggests this isn't true now in the UK (e.g., http://www.theukcardsassociation.org.uk/faqs/ ) and I can't find any evidence it was true in the past.

This is mostly false. In the past, the liability was completely on the bank. In October, it switched to the merchant only if the merchant hadn't upgraded to a chip reader. The switchover process is continuing, and when it is complete the liability will be with the banks, as it was before.

It's been a while, but I seem to recall in a past company that for card-not-present transactions, the risk of fraud was on us, not on the bank approving the transaction.

Chip and pin does not predate the EU. Debit cards used to be swipe and pin since the 80's, credit cards were not so widely used and supported both pin and signature.

I don't doubt that that many complicated economic and political factors influenced things, but you're interpreting the fraud data wrong. The US credit card fraud rate as a fraction of transactions value is currently only double (~2.1 times) the EU rate, and only 1.5 times the UK rate:

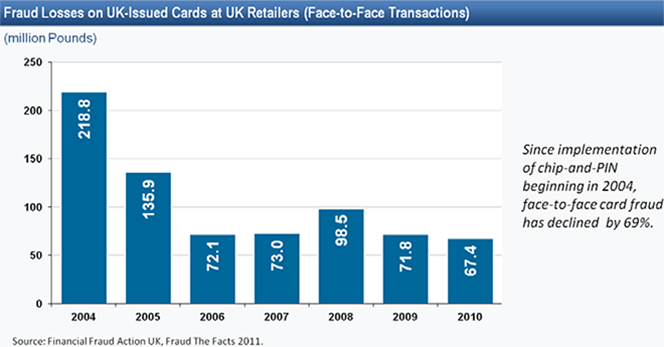

I am unable to find good data on fraud rates in Europe going back before chip-and-pin, but the system reduced fraud in the UK by ~60-70%, at least for face-to-face transactions:

So the UK almost certainly had significantly higher fraud than the US before rolling out chip-and-pin. If

seliopou is right, then this was also true for France.

Let me know if you can find better Europe-wide data.

Interchange fees are set based (in large part) on how much fraud the processor expects to deal with. This is why interchange fees are lower for card-present than card-not-present transactions, and higher in business categories that tend to have more fraud.

A processor does not charge lower fees for chip cards in a vacuum, they do it because they expect to eat less fraud from chip cards.

Oh, I understand what you're claiming now. But I don't think the effect your describing is very important. As colechristensen points out, the fees in the US are 5-20 times larger while their fraud rate is only about twice. So it looks like other factors (e.g. degree of regulation, monopsony effects, etc.) have a much larger influence on interchange fees than fraud rates. Indeed, the amount lost from fraud is only about 0.1% of transactions in the US, and 0.05% in the EU.

7-Eleven and Post Offices are the only places which accept cards issued outside of Japan. I assume they have to cover all possible types of cards, otherwise people from other countries could get stuck without money here that way.

The international ones (every 7-11 atm) have to accept everything. My Japanese card doesn't even have a magstripe, only chip and pin, so the hometown banks aren't as stupid as this may make them seem.

South Africa has had chip-and-pin cards for a very long time, but like many other countries the magstripe was kept for compatibility with US cards (I was told). I used to think this was common the world over. Not so?

Fax machines are still present pretty much everywhere, especially in corporations and government facilities. When I've been working in the UK 5 years ago in a large research institution, I had a fax machine next to my desk.

(The only thing it did though was activating once a day and printing out some ads, mostly car dealerships or insurances, AFAIR.)

I used to help my dad identify senders of spam faxes so we could get a court to issue summary judgment. I think the fine can be tripled if the violation is willful.

Even with faxes from a whole bunch of his clients... as many as I could trace back to the sender, and then of course collecting the judgment isn't easy. So after all that, it was barely enough to pay me. I guess that is why you don't see folks going after the spammers as much.

I don't know. But the first time I saw it happening I went and shown it to my boss; she reacted like most people react to on-line ads. "Yeah, it does that."

Contactless only lets you spend 25 pounds(so I guess $30-40) in a single transaction, you can only do 5 a day(until you have to enter the pin), and it's impossible to withdraw cash using it. The card also won't surrender its data without a valid decryption key from an authorized terminal. I have absolutely no idea how you can even describe contactless as "worse" in this case.

{kind=link}